Target Date Funds and Fiduciary Obligations

Published by

RPAG®

on

Target date funds (TDFs) — which rebalance investments to become more conservative as a fixed date approaches — are a convenient way for plan participants to diversify their portfolios and reduce volatility and risk as they approach retirement, making them an increasingly popular choice. However not all TDFs are created equal, and selecting and monitoring them can pose unique challenges for plan sponsors and fiduciary advisors.

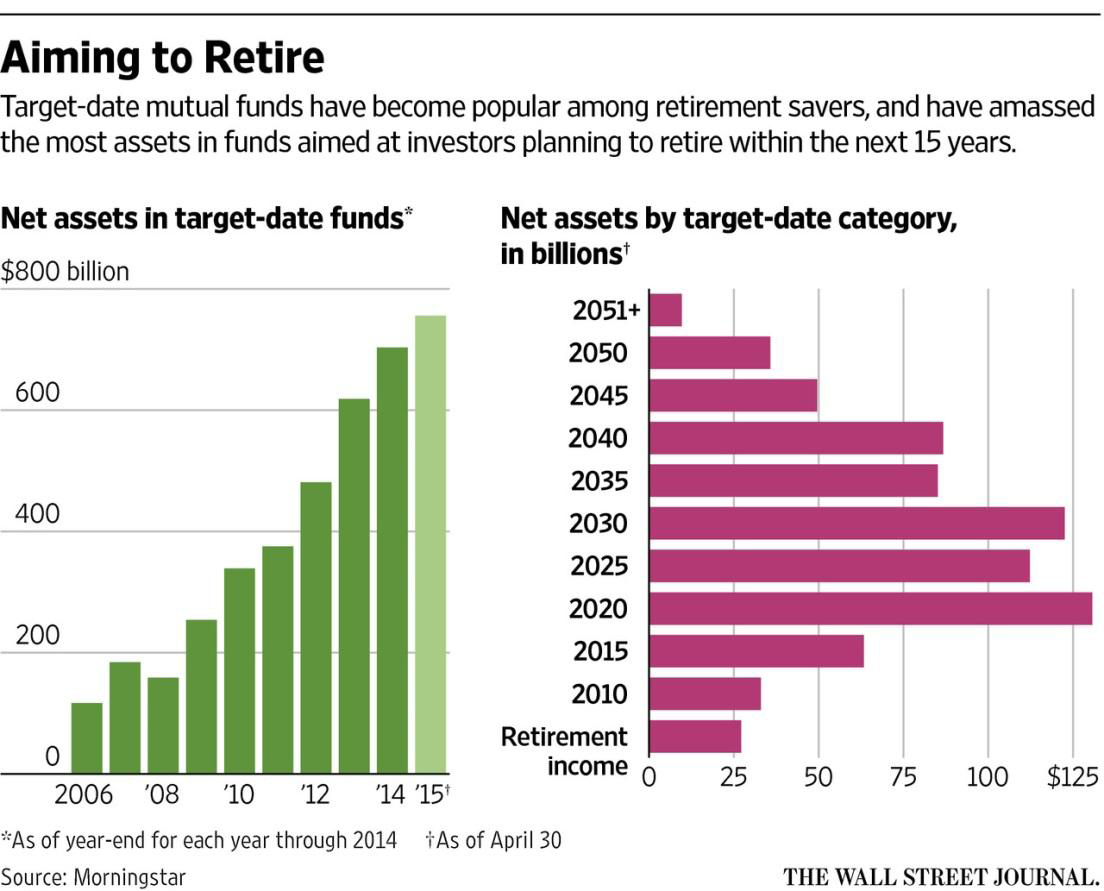

TDFs were first introduced in 1994. A little over ten years ago, just 13% retirement plan participants were invested in TDFs. Today, that number has risen to more than 50%, according to a new report from Vanguard, which also estimates that 77% of Vanguard participants will be invested in a single TDF by 2022.

However, the “automatic” rebalancing feature of TDFs doesn’t supplant the obligation to monitor funds and educate participants. The Department of Labor (DOL) provides guidance on TDFs in the form of tips for ERISA plan fiduciaries. A fiduciary advisor can help plan sponsors understand the rules and assist with compliance.

TDF Tip Highlights

- Establish an objective process for comparing and selecting TDFs. Some of the things DOL suggests you consider include: fund performance, fund fees and expenses and how well the fund’s characteristics align with your employees’ ages, retirement dates and salaries.

- Establish a process for periodic review of your plan’s TDFs. If there are significant changes in any of the criteria you considered when you added the TDF - management staff of the fund, performance, objectives - consider replacing it.

- Understand the fund’s investments and how these will change over time. Aside from the primary strategy and underlying risk, another important aspect to consider is the fund’s “glide path.” Some TDFs reach their most conservative state closer to the target date, while others continue to become more conservative as participants move through their retirement years, with the assumption that funds will be withdrawn over a longer period of time.

- Review the fund’s fees and expenses. Even small differences in fees can have a large impact on the growth of participants’ savings over time. In addition to fees and expenses charged by the component funds held by the TDF, are there additional charges for rebalancing or other services?

- Ask whether a customized TDF that includes component investments not managed by the TDF vendor would be better for your plan. There may be additional costs associated with a custom TDF, but it may be worth it and you should ask the question.

- Develop effective communications about TDFs for your plan participants, especially disclosures required by law. Check EBSA’s website for updates on regulatory disclosure requirements.

- Use available sources of information, such as commercially available resources and services, to evaluate and review TDFs as well as any recommendations received concerning their selection.

- Document your process for choosing and reviewing TDFs, including the decision-making process regarding individual investment options.

*Read the full DOL Target Date Retirement Funds — Tips for ERISA Plan Fiduciaries document here https://www.dol.gov/sites/default/files/ebsa/about-ebsa/our-activities/resource-center/fact-sheets/target-date-retirement-funds.pdf)

The trend toward TDFs has changed the landscape for retirement plan investors, and it’s a trend that shows no signs of slowing down anytime in the near future. For assistance navigating this relatively recent evolution in retirement planning and investing contact your plan advisor.

- https://www.dol.gov/sites/default/files/ebsa/about-ebsa/our-activities/resource-center/fact-sheets/target-date-retirement-funds.pdf

- https://pressroom.vanguard.com/news/Press-Release-Vanguard-Launches-How-America-Saves-2018-060518.html

- http://www.ucs-edu.net/cms/wp-content/uploads/2014/04/I_ABriefHistoryOfTargetDateFunds.pdf

The target date is the approximate date when investors plan to start withdrawing their money. Generally, the asset allocation of each fund will change on an annual basis with the asset allocation becoming more conservative as the fund nears the target retirement date.

ACR#337588 01/20